What Is The Average Retirement Age In The UK? (Updated 2026)

Retirement is a challenging subject to discuss. On the one hand, retirement is the age at which you feel comfortable and secure, cutting off your working life and living off investments, pensions, and other sources of income accrued over your working years.

Some people make a bet when they’re young; it pays off, and they can “retire” as early as their 30s. Others reach “retirement age” and continue working out of need, as their financial security isn’t guaranteed.

On the other hand, specific legal definitions of retirement and retirement age relate to your state pension and your eligibility for various social programs and safety nets.

This means that the retirement age you reach in practice may differ from the retirement age the government has set.

That said, the retirement age at which you feel financially secure enough to stop working isn’t as relevant to this guide as the other official retirement age.

The official retirement age determines many different things about how you can qualify for and receive your state pension, so it’s important to know, regardless of your specific financial situation.

The Cultural and Social Retirement Age

Before discussing what the law and the government say about the retirement age, it’s also worth taking a look at the social and cultural retirement age.

In other words, despite what the government sets as policy, what is the age at which people are retiring?

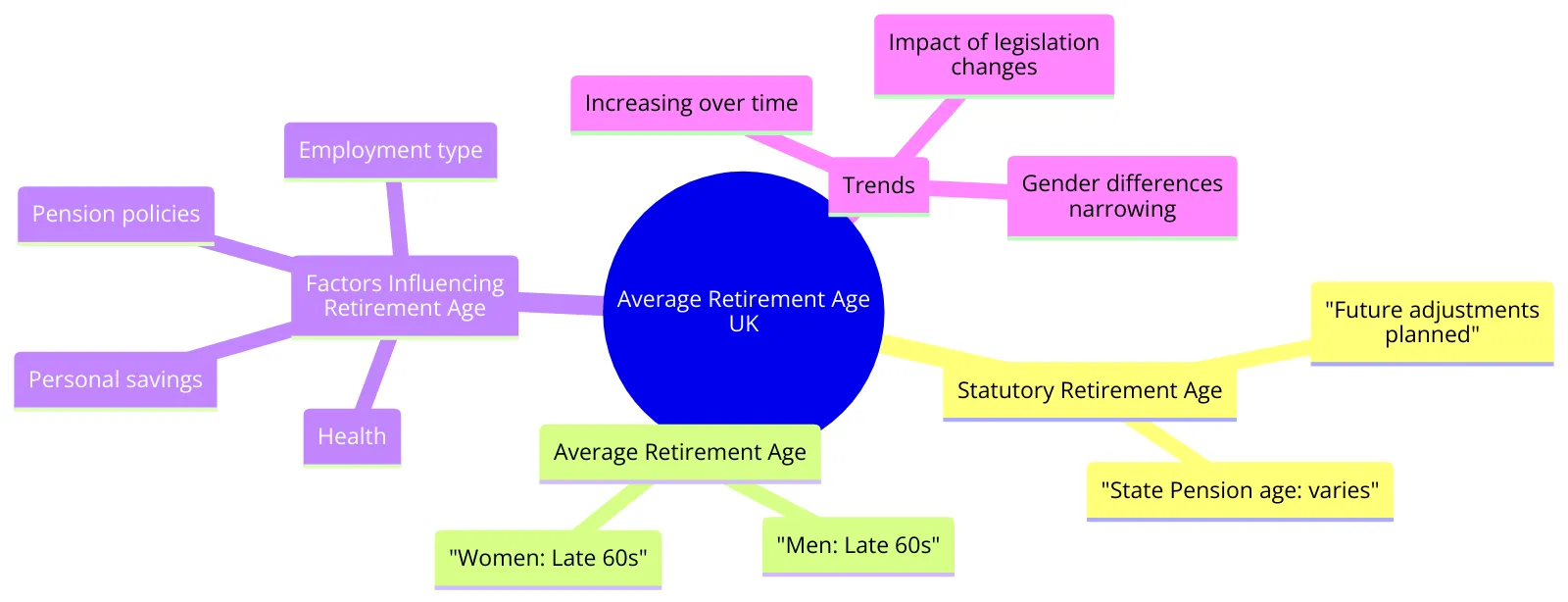

As of 2026, the average retirement age for men is slightly over 65, which is right around the government’s long-set retirement age.

For women, meanwhile, the average retirement age is slightly earlier, at 64. Both of these numbers are slightly lower than they have been in the past, indicating that people are retiring slightly earlier than before, but not by much.

Keep this in mind as you read the remainder of this article and consider the potential implications for your own retirement.

At What Age Do People Actually Retire? – Insights into Retirement UK Trends

The Default Retirement Age

You may have heard of (or had family members suffer from) the Default Retirement Age, or DRA.

The DRA was the age at which the government said an individual would be able to retire to live out their golden years. More importantly, it was the age at which companies were allowed to force their employees to retire.

That age was 65. Two factors led the government to reconsider this (and you may note the use of the past tense in the preceding paragraph): increasing life expectancy and quality of life over time, and corporate abuse.

In the past, for example, in the 1950s, when average life expectancy was around 70, retiring at 65 and spending the last few years of your life receiving government pension benefits was perfectly acceptable.

Over time, though, advances in the world, workplace safety regulations, the health of our food and water, and even medical care have all made great strides in increasing life expectancy.

These days, instead of 70, it’s closer to 81, and projections indicate that by 2070 it could reach 92.

For the government, this is almost a crisis. It’s one thing to plan around paying for 5-10 years of the elderly’s lives; it’s another to confront the need to support 20-30 years of life.

Meanwhile, companies were more than happy to enforce the default retirement age and force out their older employees at 65, replacing them with younger (and less well-paid) employees.

This left people in potentially tough situations: they were too old to be employable but hadn’t amassed enough savings and investments to survive.

In 2011, the government abolished the default retirement age. This does not mean there is no official retirement age; however, companies are no longer required to retire anyone who reaches that age.

While some companies can still enforce a compulsory retirement, they must prove it’s warranted, such as in cases where peak physical performance and reaction times are necessary.

The State Pension Age

We’ve mentioned that there’s still an official retirement age; this is the state pension age.

The state pension is something we all pay into as we go about our working careers, and once we reach a specific age, we can start receiving disbursements from it. In the past, this was meant to replace income and allow retirees to live without having to work.

Today, it’s often more supplemental, allowing older people to reduce their working hours or transition to more hobby-focused or passion-project secondary income supplemented by the pension.

This age is periodically adjusted to account for increases in life expectancy. As people are expected to live longer, pensions are stretched thinner or run out sooner, leaving the elderly in a difficult situation.

While it may feel bad to have your target retirement age raised just a few years before you reach it, it’s no better to reach your twilight years and run out of money to survive, either.

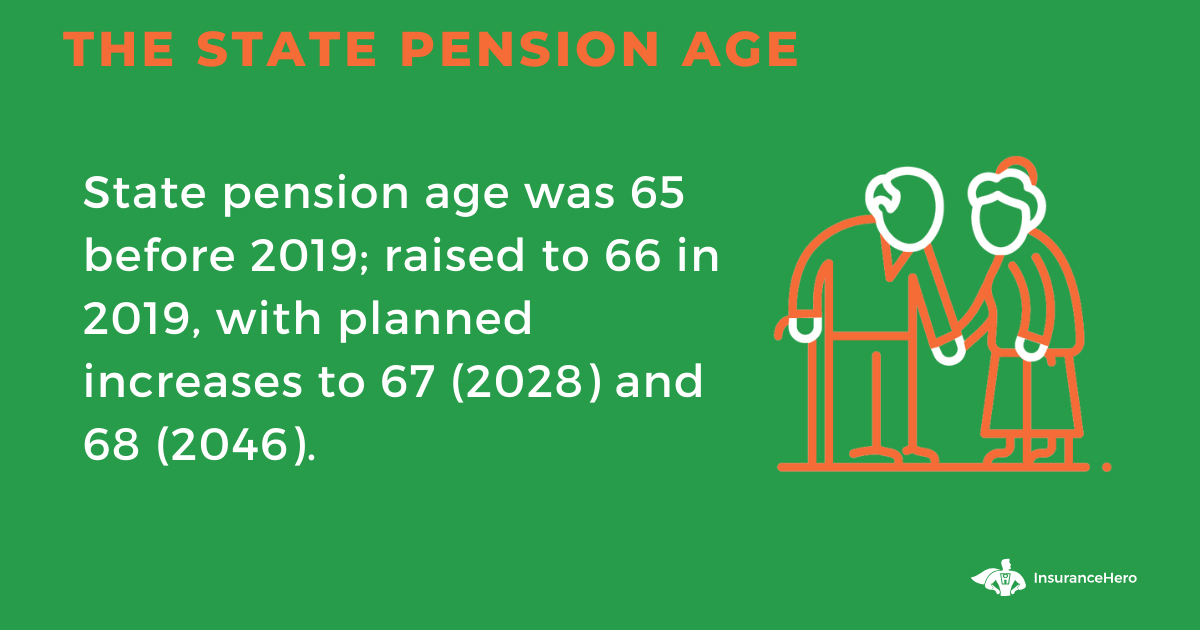

The state pension age was 65 before 2019. In 2019, it was raised to 66, which is where it is currently.

The government legislation that changed it is part of an ongoing adjustment planned for the next several decades.

The plan is to raise the age to 67 again in 2028, and then to 68 in 2046.

This is a straightforward calculation for many, but for some on the cusp of retirement in one of these transition years, it can be challenging to determine when exactly your state pension will kick in.

Fortunately, the government offers a simple calculator here. Input your date of birth, and it will tell you the date you will be eligible to receive your state pension and any potential credits or additional support you may qualify for.

To be clear: you can retire at any time, before or after your state pension age. Some people retire as early as 55 for a “normal” retirement; others retire even earlier when their finances allow. Others keep working longer, and may not retire until 70 or later. The State Pension Age is the minimum age at which you can start taking your state pension.

You can, if you choose, wait several years to start drawing on your state pension. Additionally, suppose you have a serious injury or ill health.

In that case, you may be eligible to retire anytime and even take 100% of your eligible state pension as a single lump sum.

One important note is that the amount you can receive from your state pension depends on the number of qualifying years of work in the UK.

If you retire early, you may not have a “full” state pension because you didn’t reach the maximum number of qualifying years.

If you are still young and plan to retire early, you may be able to add additional voluntary contributions to accrue qualifying years at a rate faster than one year per year. These are also called NICs (National Insurance Contributions), and you can learn more here.

The Average Retirement Age In The UK Mind Map

Impact on Retirement Income

| Factor | Description |

|---|---|

| State Pension Age Increase | As the state pension age increases, people may need to work longer to qualify for full pension benefits, potentially affecting their retirement income. |

| Personal Pensions | The age to access personal pensions is set to increase from 55 to 57 in 2028, affecting when individuals can start drawing from these funds. |

| Retirement Income Expectations | With the average expected retirement age shifting, individuals’ retirement income planning must adapt, considering UK state and personal pension adjustments. |

Retirement and Personal Pensions

Your state pension isn’t the only form of retirement income you must consider when planning the latter portion of your life.

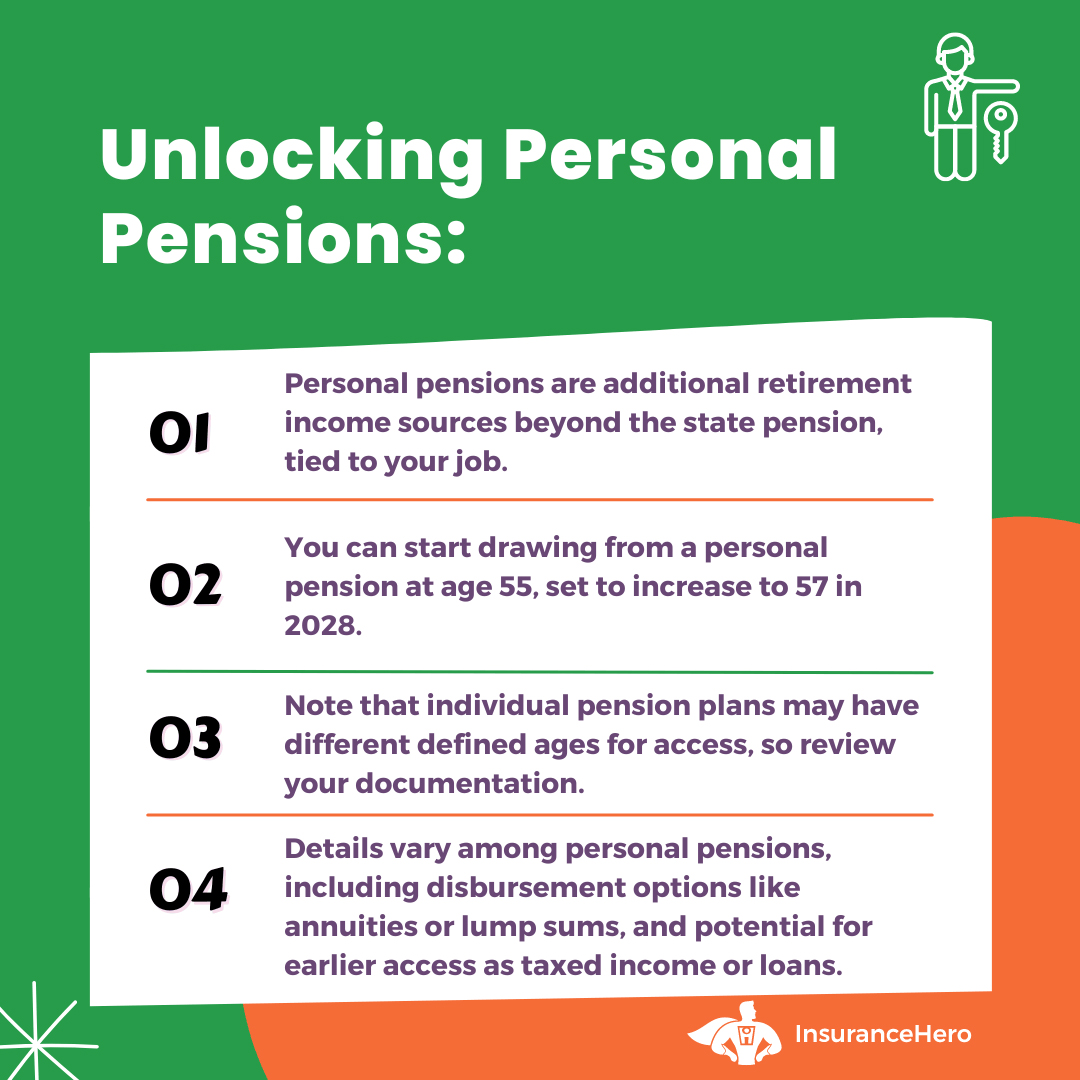

There are also personal pensions, which are generally personal accounts tied to your job, which you pay into as you work, and you can start drawing from them once you reach a defined age.

Like your state pension, you can start drawing upon a personal pension at a specific age. Also, like the state pension, this age is slated to increase over time. Unlike state pensions, however, the age is earlier.

Specifically, personal pension age is currently 55, and is slated to increase to 57 in 2028.

The trick is that this isn’t universally true; some personal pensions have defined ages other than the general pension age, and you’ll need to check your documentation to know for sure.

There are also a lot of details that vary between individual pensions, including whether or not it’s in the form of an annuity, whether you can take some disbursement as a lump sum when you reach the qualifying age, and whether or not you can take earlier disbursements as taxed income or as a loan you repay.

Retirement is Changing — Is Your Family’s Future Secure? Get Life Insurance Quotes In Minutes

Retirement Income In 2026

The tables below provide a snapshot of the current state of retirement income in the UK, including average incomes for retirees, the income needed for different lifestyles, and comparisons between state pensions and average retirement incomes.

The data reflects the latest figures as of early 2026.

Average Retirement Income in the UK

| Status | Weekly Income (£) | Annual Income (£) |

|---|---|---|

| Retired Couple | £511 | £26,572 |

| Single Retiree | £246 | £12,792 |

Required Retirement Income for Different Lifestyles

| Lifestyle | Single Person Annual Income (£) | Couple’s Annual Income (£) |

|---|---|---|

| Minimal | £12,200 | £15k+ |

| Comfortable | £30,000 | £49,500+ |

| Luxury | £35,000+ | £55,000+ |

State Pension vs. Average Retirement Income

| Description | Amount (£) |

|---|---|

| Full UK State Pension | £10,600 |

| Average Retirement Income (Single Pensioner) | £12,800 |

Future Uncertainty in Retirement

It’s worth mentioning that there is a lot of uncertainty about the state of the world and the future of economics right now.

In particular, various unusual factors are coinciding to skew the long-term predictions that many factors rely on, such as the government’s decision to increase retirement age.

These include the following:

- The increasing effects of climate change are causing unseasonable weather shifts, disrupting everything from property values to labour stability to the viability of entire industries.

- The COVID-19 pandemic has killed nearly a quarter of a million people, many of whom statistically wouldn’t have passed so early, skewing life expectancy numbers and the balance of pension funds.

- After Brexit, the UK’s role in the greater global economy and the stability of its populace are dramatically uncertain.

There’s no way to tell yet what effects these will have on the long-term planning for the state pension and designated retirement ages. Suffice it to say that the future is, as always, uncertain.

The Average UK Pension – Have You Saved Enough For Retirement?

The UK Government State Pension Age Review 2023 – In Summary

The key findings and recommendations are based on the State Pension Age Review 2023 report.

Executive Summary

- Objective: Second Review of State Pension age by the Secretary of State for Work and Pensions, as required under the Pensions Act 2014.

- Key Findings:

- Life expectancy has increased significantly over time, but the rate of increase has slowed since the 2017 review.

- The projected life expectancy by 2070 is 92.5 for males and 94.6 for females.

- The demographic shift will result in 5 million more pensioners by 2070, significantly impacting the pensioner-to-working-age population ratio.

- State Pension costs are projected to rise from 4.8% of GDP in 2021-22 to 8.1% in 2071/72.

Recommendations

- Proportion of Adult Life in Retirement:

- It remains appropriate to have a fixed proportion of adult life spent in retirement, recommended at ‘up to 31%’.

- The increase in State Pension age to 67 from 2026 to 2028 aligns with this proportion.

- Recommendations suggest deferring the decision to increase the State Pension age to 68 until more accurate data is available.

Conclusions and Actions

- Immediate Actions:

- The rise of the State Pension age from 66 to 67 between 2026 and 2028 is confirmed as appropriate.

- A further review, considering the latest information and data, will be conducted within two years of the next Parliament and will consider the rise to age 68.

Future Considerations

- Review Focus:

- The following review will include updated life expectancy and population projections, economic assessments, and labour market impacts.

- The government remains committed to providing ten years’ notice for any changes to the State Pension age.

Data Tables

Table 1: Projected Life Expectancy Changes

| Year | Male Life Expectancy at Birth | Female Life Expectancy at Birth |

|---|---|---|

| 1951 | 66.5 years | 71.5 years |

| 2020 | 79.5 years | 83.1 years |

| 2070 | 92.5 years | 94.6 years |

Table 2: Pensioner to Working-Age Population Ratio

| Year | Pensioners per 1,000 Working-Age Population |

|---|---|

| 2020 | 280 |

| 2070 | 393 |

Table 3: State Pension Costs as % of GDP

| Fiscal Year | % of GDP |

|---|---|

| 2021-22 | 4.8% |

| 2071-72 | 8.1% |

Insuring Against an Uncertain Future

While pensions and other investments are meant to pay out when you reach an old enough age that you can no longer work but still need to be supported somehow, they tend to have one significant limitation: they end when you do.

While this isn’t necessarily bad on the face of it, the government has no reason to continue paying a pension to someone who isn’t alive to use it. It does leave families in a bind.

Your spouse, your children, and your loved ones may all rely on your support to maintain their standard of living.

In our modern world, often, one pension isn’t enough to cover living expenses for a couple of pensioners, while the combination of both of their pensions will.

So when one individual dies and their pension stops, what does the other spouse do? What does the family do?

There are some mechanisms in place to assist with this. State pensions can be partially inherited by a spouse, and personal pensions may be cashed out as a lump sum and included in the estate.

Unfortunately, these aren’t always enough to replace the lost income, especially if the person who passed away was also still working as a supplement. So what can you do?

The answer is life insurance. Purchasing a life insurance policy is a very minimal monthly expense. Still, it costs a significant amount of money that, upon the individual’s death, will be paid out to their loved ones.

There are three major benefits to this:

- A life insurance policy can pay out to more than just a spouse; it can be paid to children, grandchildren, business partners, a charity, or virtually any entity you choose to label your beneficiary.

- Life insurance cover is available no matter how old you are, and there are even guaranteed policies for those over 50.

- It’s easy to find and sign up for life insurance coverage, even for those over 70 years old.

- Two insurers are particularly relevant in this case: one is British Seniors, and the other is AXA.

People who have a private pension and can afford to make monthly payments on a retired person’s insurance policy could save money by getting cover before you are over 65 and getting an over-60 policy instead.

If you’re interested in providing additional support for your family and loved ones after you pass away and want to ensure you’re doing so in the best way possible, we’re here to help.

Instead of manually finding insurance companies, asking them for quotes, and figuring out the best options, we help you do all that in one quick form.

Fill out this form, and all of the UK’s top insurance providers will offer you their best quotes so you can evaluate and pick the best one to secure your family’s future.

Research data sources:

- https://www.lse.ac.uk/study-at-lse/Undergraduate/Assets/PDF/UGAA-English-Section-A-2022.pdf

- https://www.simplybusiness.co.uk/knowledge/articles/retirement-age-uk/

- https://www.gov.uk/government/publications/state-pension-age-review-2023-government-report/state-pension-age-review-2023

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.