Life Insurance For Inheritance Tax Planning After 60

Many people think that inheritance tax (IHT) only affects the wealthy. Still, with increasing house prices and inflation surging asset values, more people are impacted by it than they might realise.

It can significantly reduce the legacy you plan to leave your loved ones.

A great way to manage the cost of IHT is to get life insurance for those over sixty in the UK to provide your beneficiaries with a tax-free death benefit they can use to cover any tax obligations.

You can find out if you need life insurance for inheritance tax planning after sixty by appraising your estate’s worth and estimating your possible IHT.

Then, you can obtain life insurance to pay out an amount that can cover that bill.

60 Or Over And Need Life Insurance? Get A No-Obligation Quote Today

| Consideration | Our Explanation |

|---|---|

| Purpose | Life insurance can provide a tax-free lump sum to cover inheritance tax (IHT) liabilities. |

| Age Consideration | After age 60, premiums may be higher, but coverage is still possible depending on health and policy type. |

| Policy Type | Whole of life insurance is commonly used for IHT planning because it guarantees a payout whenever you die. |

| Underwriting | Medical underwriting is usually required. Some providers offer guaranteed acceptance plans with higher premiums. |

| Trust Placement | Placing the policy in a trust ensures the payout isn’t part of your estate, helping avoid additional IHT. |

| Joint Policies | Couples often use a joint life second death policy, which pays out after the second person dies, when IHT is typically due. |

| Premium Affordability | Ensure premiums are sustainable long-term, especially on fixed income during retirement. |

| Tax Efficiency | Payouts are typically not subject to income or capital gains tax, and trusts can avoid IHT on the benefit. |

| Advice Recommended | Consulting a financial adviser can help you tailor a policy to your estate-planning needs and ensure it’s set up correctly. Insurance Hero is more than happy to help you with this. |

| Alternatives | Gifting assets, setting up trusts, or using pension assets can complement or reduce the need for life insurance in IHT planning. |

Understanding Inheritance Tax

Inheritance tax is a tax paid on the value of your estate when you pass away. Your estate can include your properties, savings, investments, and other assets such as jewellery, art, and cars.

IHT usually applies to any assets that you intend to leave to friends and family, excluding spouses and partners, but including children.

In the UK, IHT accounts for 40% of the total value of assets exceeding £325,000.

You can reduce the payable rate to 36% if you donate at least 10% of the value of your estate to charity, as donations of this nature are not subject to IHT.

The Importance of Inheritance Tax Planning

Inheritance tax planning is the process of laying down safeguards to ensure that IHT is minimised, allowing your loved ones to enjoy your legacy in full.

Paying IHT is also an essential step to releasing your estate; without settling the bill, your family won’t be able to access your assets.

Do I Need to Pay Inheritance Tax?

- You can determine if you’re subject to IHT by determining your estate is worth. Add up all your assets, then deduct any outstanding debts, gifts, charity donations, and end-of-life expenses.

- If the value of your estate is less than £325,000, you don’t have to pay any IHT. Otherwise, your loved ones could expect a tax bill upon your death, with any amount above £325,000 subject to inheritance tax.

Life Insurance and Inheritance Tax Planning

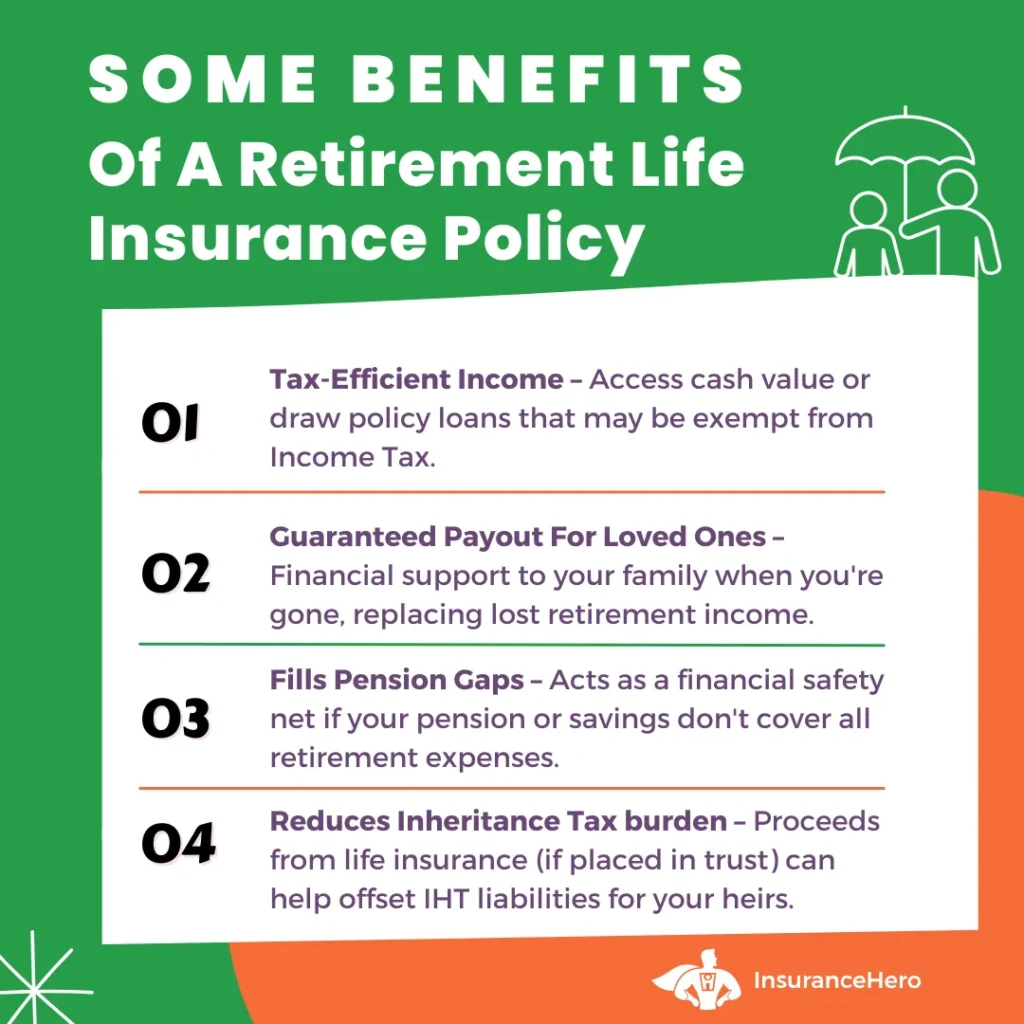

Life insurance after sixty can be helpful for inheritance tax planning because your beneficiaries can use its payout to cover IHT.

Life insurance benefits are also typically quickly distributed, so your loved ones can enjoy their inheritance sooner.

You should speak with a financial planner or contact Insurance Hero to ensure that your life insurance is structured correctly and can be used in this manner after your death.

They can also answer some frequently asked questions about senior life insurance, including how medical exams impact life insurance rates for seniors over sixty and how to use life insurance as an income replacement after retirement.

Writing Life Insurance in Trust

Technically, the payout from your life insurance policy is considered part of your estate. That means it could also be subject to IHT, removing a significant sum from what could have been paid upon your death.

However, you can avoid IHT being charged on your life insurance policy by writing it ‘in trust.’

A trust is a legal arrangement that appoints trustees, such as a solicitor, to look after an asset on behalf of your beneficiaries until they intend to benefit from it.

When you write your policy in trust, the payout goes directly to your beneficiaries instead of becoming a part of your estate, removing any IHT due.

Life Insurance for Inheritance Tax Planning After Sixty

If you’re considering protecting your legacy, consider using life insurance as an inheritance tax planning tool.

Compare your options for life insurance for those over sixty in the UK and get a personalised quote from Insurance Hero today.

Research sources and resources you may find helpful

- https://connect.avivab2b.co.uk/adviser/articles/tech-centre/protection-planning/personal-protection/life-assurance-for-inheritance-tax-planning

- https://adviser.royallondon.com/articles-and-guides/protection/using-a-whole-of-life-plan-when-inheritance-tax-planning/

- https://www.moneysavingexpert.com/family/inheritance-tax-planning-iht/

- https://www.zurichintermediary.co.uk/advice-matters/giving-advisers-another-tool-in-their-estate-planning-toolkit

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.