How Medical Exams Impact Seniors Over 60 Life Insurance Rates

If you’re contemplating getting life insurance, you might be worried about how your medical exam could affect your rates.

Medical exams are important to life insurance policies because they can help determine the insured’s state of health, pre-existing conditions, and life expectancy.

These are factors that insurance companies use to calculate premiums.

When shopping for life insurance for those over sixty in the UK, knowing what to expect from a medical exam and whether you should try to avoid one can be helpful.

60 Or Above And Need Life Insurance Without A Medical? Get A No-Obligation Quote Today

| Factor | Impact On Premiums For People Over 60 |

|---|---|

| Medical Exam Required | Typically results in lower premiums if the senior is healthy. |

| No Medical Exam | Often leads to higher premiums due to increased insurer risk. |

| Health Conditions Identified | Depending on severity, it can increase rates or lead to coverage denial. |

| Favourable Medical Results | May qualify the applicant for preferred or standard rates. |

| Extensive Medical History Review | Helps insurers price the policy better, possibly lowering rates. |

| Limited Medical Information Provided | May result in higher premiums or reduced policy options. |

What to Expect During a Medical Exam

First, let’s know what we’re talking about when we discuss medical exams required by insurance companies.

Usually, the process isn’t very long, but it often includes several components:

- Medical history: Applicants are asked about their current and past health conditions and to disclose family medical history. They may also be asked about their lifestyle, including diet, smoking, and drinking habits.

- Basic measurements: Information like height, weight, BMI, and blood pressure is recorded.

- Blood and urine tests: Applicants are tested for high cholesterol, diabetes, and kidney and liver health.

- EKG: For applicants over sixty, it’s not uncommon that the medical exam includes an electrocardiogram (EKG) to establish the health of their heart.

- Mental acuity: Older applicants may also be asked to complete a test that measures their cognitive ability.

Essentially, these tests attempt to capture a three-dimensional picture of the applicant.

By understanding their past and present, insurance companies try to predict the health future of the person looking to be insured.

How Medical Exam Results Can Affect Your Rates

With medical exams, insurance companies are looking for any indication of risk to the applicant.

Here are a few red flags they’re focused on:

- Heart health: Heart health can wane as people age, and high blood pressure, irregular heartbeat, or a history of heart attacks can be noteworthy to insurers.

- Diabetes: Even if an applicant has shown to have few side effects from diabetes until now, it can increase their risk of future health complications.

- Cancer: Similarly, even if an applicant is in remission, the details of their history with cancer can affect their premiums.

- Obesity: About a quarter of people in the UK are obese, and because of the risks it poses to an applicant’s health, obesity matters to insurers.

The reasons for red flags can be diverse, but the outcome is almost always the same: any of these risks present in the applicant will likely increase their insurance premiums.

Guaranteed Life Insurance

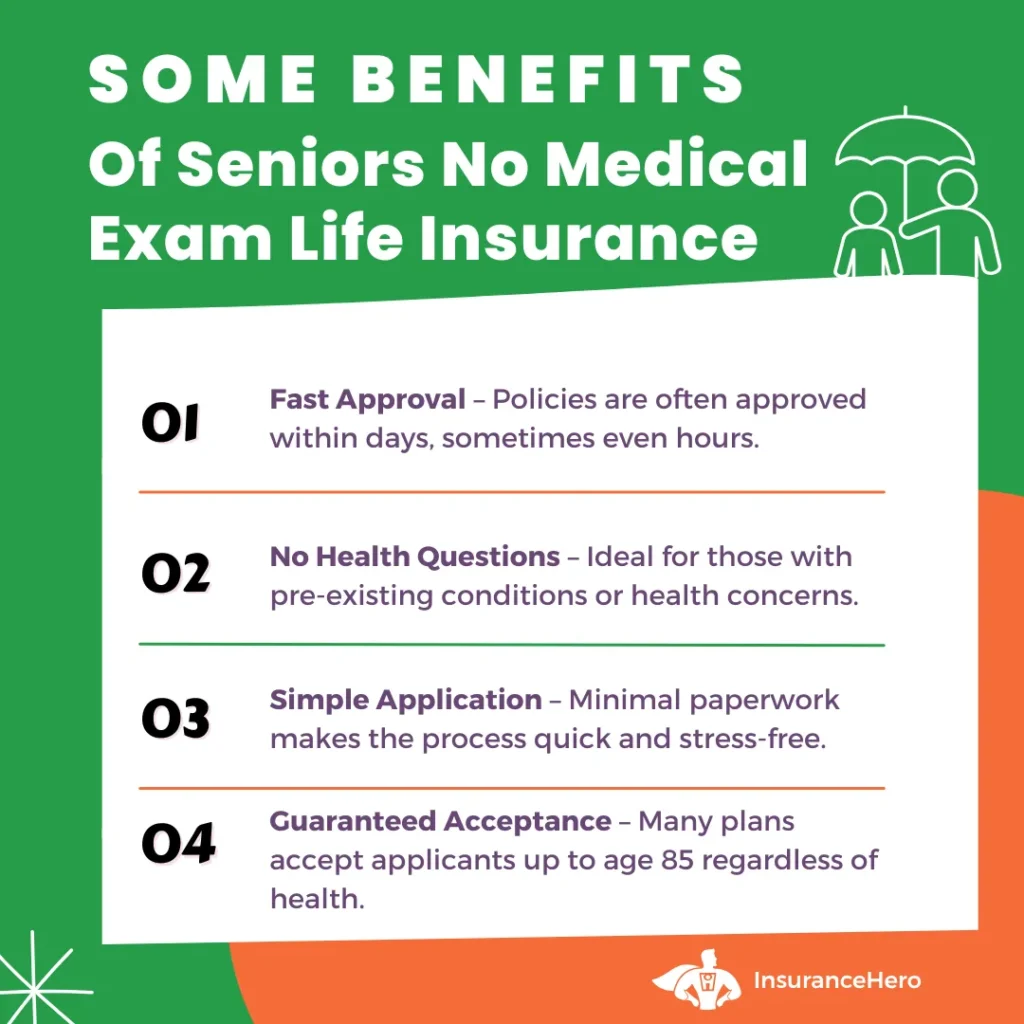

If you want to avoid a medical exam for any reason, you can consider applying for guaranteed life insurance.

These policies are targeted towards seniors and don’t require any health information to be shared with providers beforehand.

However, they can come with higher premiums and lower payouts, so they aren’t a good fit for everyone.

This type of coverage is also sometimes relevant to how seniors over sixty use life insurance to mitigate inheritance tax.

Life Insurance for Over 50s

This type of cover is a popular option among older adults in the UK. It usually doesn’t involve any medical tests or in-depth health questionnaires.

Most providers offer guaranteed acceptance to UK residents aged between 50 and 80, and sometimes up to 85, no matter their health condition.

Waiting Periods

Policies that don’t require a medical exam usually have an initial waiting time, often between one and two years.

During this period, if the policyholder passes away from natural causes, the payout may be limited to a refund of premiums paid.

Full coverage typically only applies to accidental death during this time.

Why it Matters

Insurance can sometimes feel complicated, and if you’re over sixty, insurers might try to find ways to charge you the highest premium possible.

Life insurance is important to provide for your family and your future, but the number of options can be overwhelming.

Insurance Hero can help you compare providers and get you a personalised quote so you can find the best coverage for you.

If you want to learn more about how life insurance can help you and your loved ones, check out our report on determining if you need life insurance for inheritance tax planning after sixty.

Further resources we hope you find helpful:

- https://www.moneyhelper.org.uk/en/pensions-and-retirement/taking-your-pension/early-retirement-because-of-illness-sickness-or-disability

- https://oneyou.southglos.gov.uk/wp-content/uploads/sites/414/2019/02/NHS-Health-Check-Patient-information-leaflet.pdf

- https://www.vitality.co.uk/life-insurance/guides/medical-records/

- https://www.legalandgeneral.com/insurance/life-insurance/health/life-insurance-no-medical/

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.