Different Types Of Life Insurance Policies 2025 Guide

About 58% of adults in the UK don’t have life insurance. This shows how important it is to know about the various life insurance options.

By researching the different life insurance types, you can choose wisely and protect your family’s financial future.

Over many years, Insurance Hero has helped homeowners and families choose the right life insurance policies in the UK.

Our experience includes guiding policyholders on Term, Whole of life, Critical illness, Mortgage life insurance, and income protection options to match their needs.

Help Safeguard Your Family’s Future Today. Find Your Cheapest Quote

What type of life insurance do I need?

To work out the types of life insurance that are best for you, you must determine your assets and liabilities and your family’s current and future shape.

It is an exercise in what if. People ask many questions, including the benefits and drawbacks of whole life insurance and whether critical illness cover is worth it.

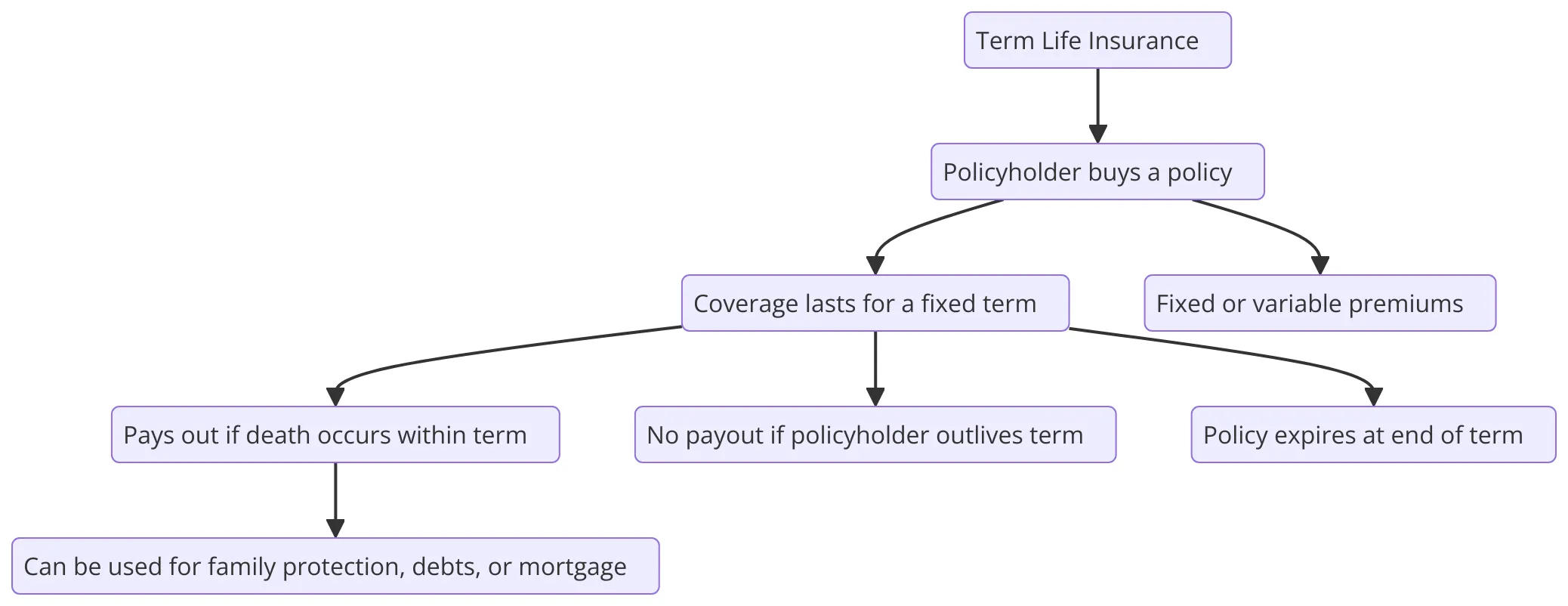

Term Life Insurance and its different types

A term life insurance policy covers you for a fixed term, usually spanning where all your significant liabilities are. This likely includes the age of your children.

Because of industry changes, Insurance Hero can offer you some new term life quotes for 2025. For some people, it may be good to terminate an old legacy policy and get a new one that is lower priced, better quality, or more suitable.

Many brokers do not offer advice, and the Insurance Hero team has often found that people have cover that is not suitable for their needs.

Decreasing Term Life Insurance

This type of policy has a slightly confusing name. Sometimes, it is called mortgage life insurance. The decreasing does not refer to the term; it refers to the cover amount.

Most people have a repayment mortgage, where the amount of money they owe goes down over time. As such, the amount the policy pays out also decreases over time.

For example, if your mortgage debt drops from £150,000 to £50,000 during the policy period, the protection amount shrinks in line with it.

This type of term insurance often costs less than level or increasing options, so decreasing term life insurance is popular among homeowners who want coverage for their remaining loan balance.

This is often the cheapest life insurance cover, but it’s inappropriate for every family.

An even more cost-effective option for some people is a joint mortgage life insurance policy where both adults are covered.

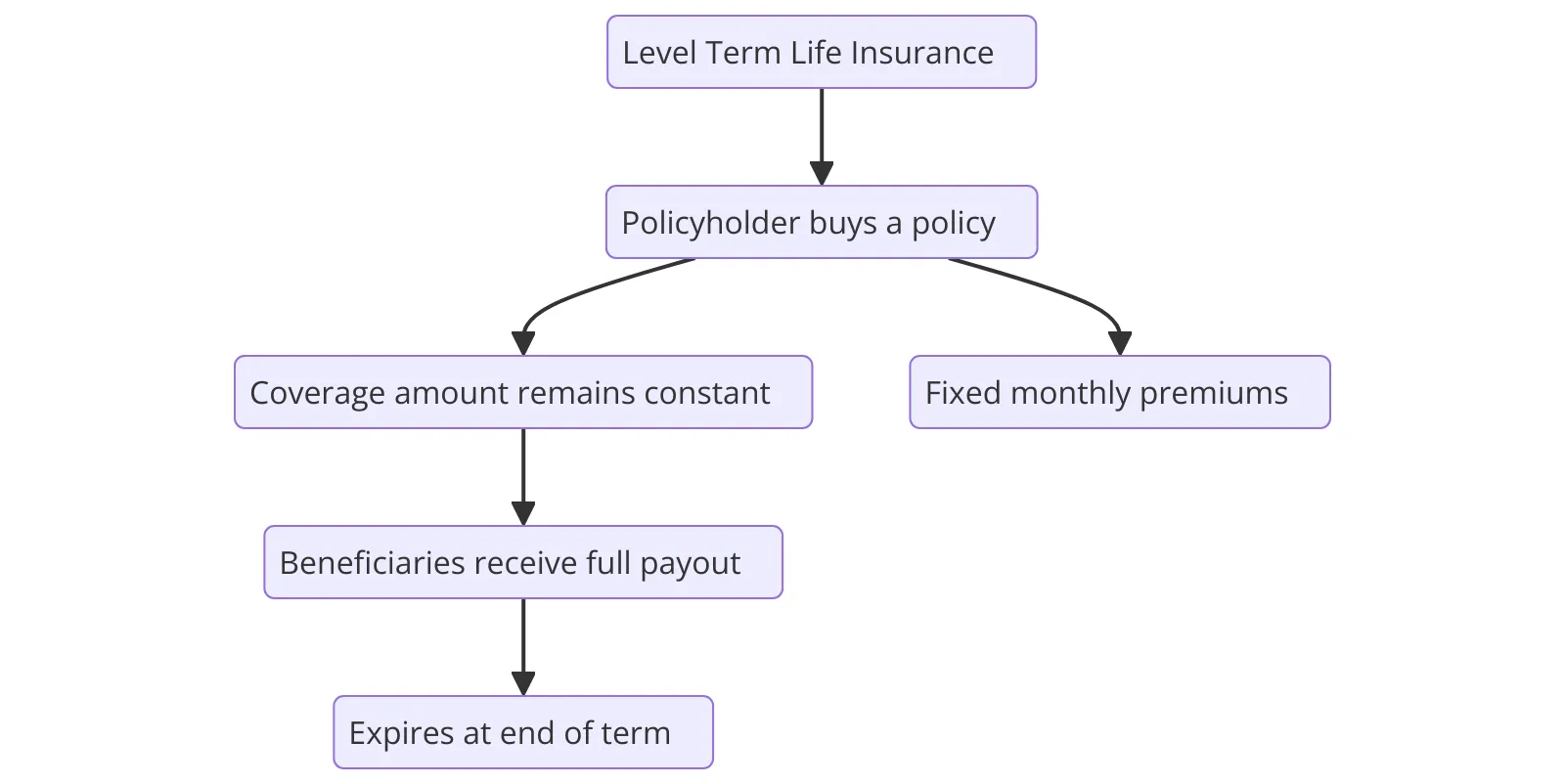

Level Term Life Insurance

It’s a common question for Insurance Hero advisors: what does level-term life insurance mean? Well, it’s simply life insurance with a fixed term that pays out a fixed amount.

Level Term Life Insurance gives a fixed payout if the insured person dies within a set time. Unlike Decreasing Term Life Insurance, where payouts shrink with loans or mortgages, Level cover stays steady for the whole term.

Premiums stay fixed, too, making it easy to budget finances and manage living costs like childcare and car insurance.

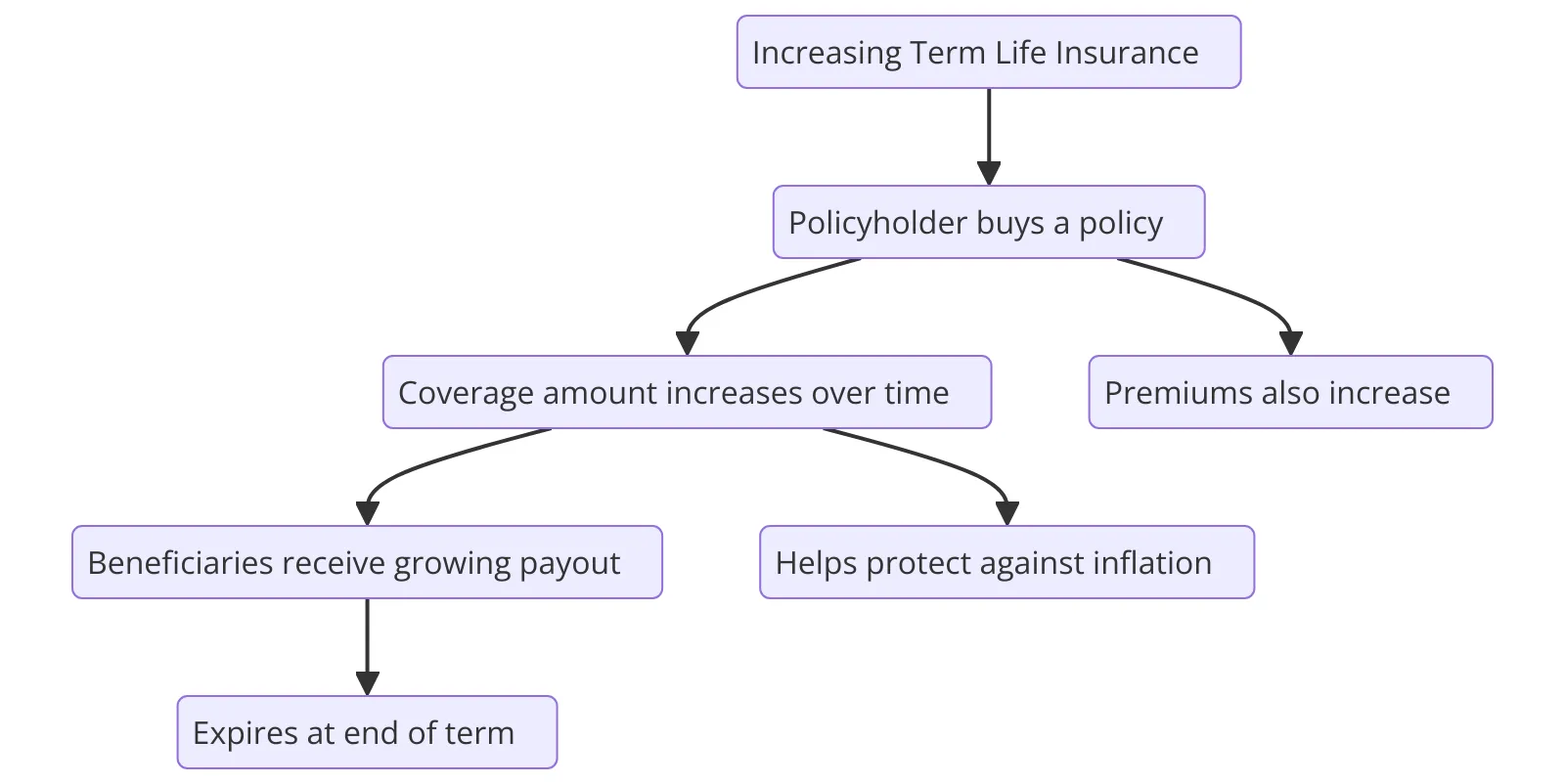

Increasing Term Life Insurance

If you want life cover that accounts for your family’s living costs, not just your remaining mortgage, increasing term life insurance could be best for you.

Did you know it’s the banker’s written policy to destroy the value of money slowly? It sounds crazy, doesn’t it? However, the Bank of England is expected to target 2% inflation.

With an increasing term life insurance policy, you pay a higher premium for the cover amount to increase over time, usually by the current level of inflation.

Whole of Life Insurance

Whole of life insurance provides cover for your entire lifetime, guaranteeing a payout upon your death. Unlike term policies that end after a set period, whole life plans offer lifelong peace of mind and often have an investment element—known as cash value—that builds savings over years.

You pay regular premiums into the policy, part of which goes towards protection, and insurers invest another portion in assets like bonds or stocks and shares ISAs.

- Cash value builds slowly but steadily, letting you borrow against it if needed.

- This type of coverage costs more than basic term cover due to lifelong coverage and cash accumulation features.

However, whole life can prove helpful for estate planning in the UK because payouts usually go tax-free to beneficiaries, easing inheritance taxation burdens families face following the loss of loved ones.

Premiums can stay fixed from day one or rise gradually based on factors such as age or health conditions assessed during underwriting by insurers within the UK’s highly regulated insurance industry.

Critical Illness Cover

Critical Illness Insurance pays out a tax-free lump sum if you receive a diagnosis of a serious illness. Common conditions covered include heart attack, stroke, cancer and major organ transplants.

- Unlike Whole Life Insurance or over-50 Life Insurance, which pay upon death, this policy helps manage financial burdens while you’re alive.

- The payout can be used for mortgage payments, income drawdown gaps due to sickness, home adaptation, or even that long-awaited campervan trip.

Policies vary widely in cost and coverage depending on personal risk factors such as age, lifestyle habits, and family medical history.

Critical illness cover from Insurance Hero can be purchased standalone or as an add-on underwritten with life insurance policies. Insurance Hero can help you compare costs and benefits carefully before you commit.

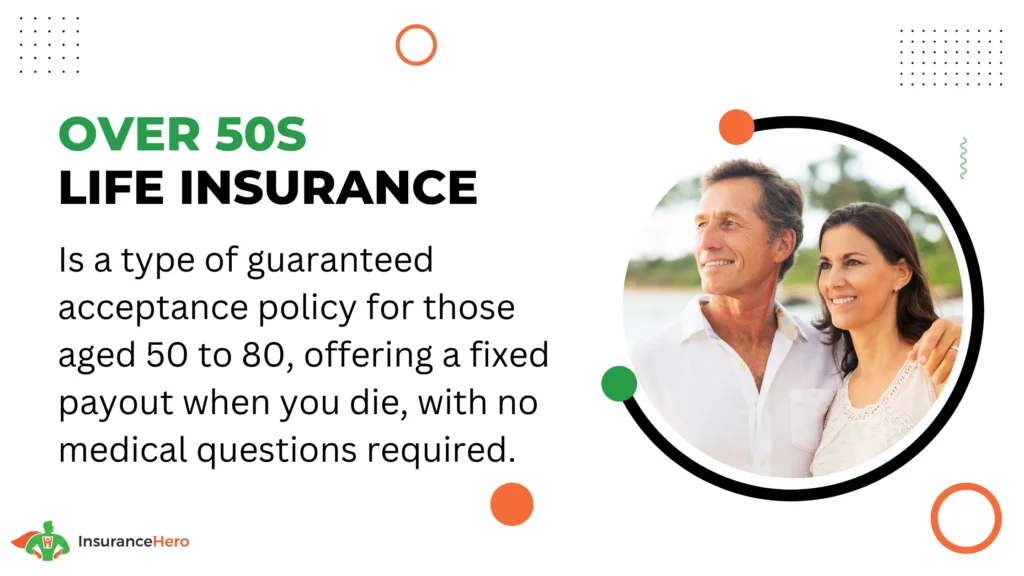

Over 50s Life Insurance

While income protection insurance covers lost wages if you fall ill, over 50s Life Insurance offers a simple way to leave money behind for loved ones.

This policy is easy, and there is no need for medical checks or questions about your health.

You pay fixed monthly payments until you reach a certain age, usually around 90, or pass away. The payout can help cover funeral costs, unpaid debts, or small gifts to family members.

However, the lump sum paid out is often relatively modest, typically between £1,000 and £25,000. This might not be enough to replace pensions or provide a large life annuity payment, but it is helpful.

Mortgage Life Insurance

Mortgage life insurance helps protect your home. It pays off your mortgage if you pass away before finishing repayments.

- This type of life insurance is usually set up as a decreasing term policy, with the payout getting smaller over time, in line with your shrinking mortgage balance.

- Most lenders suggest this cover for new homeowners taking out mortgages.

Mortgage life cover can offer peace of mind to families who rely on regular income and may struggle financially without support.

Premiums are often cheaper than level term insurance; payments decline as the amount owed on your house falls, keeping costs low and manageable each month.

Life Insurance For UK Expats

Life insurance for UK expats provides financial protection for loved ones in the event of the policyholder’s death while living abroad.

Policies can be taken out through international providers or UK-based brokers like Insurance Hero. Expat coverage usually requires medical underwriting and proof of residency.

Premiums and terms may vary based on country of residence, risk factors, and currency exchange considerations.

Factors to Consider When Choosing a Policy

Choosing the right life insurance depends on your needs, budget and future plans.

Coverage duration

Coverage duration means how long your life insurance lasts. Whole of Life Insurance covers you until death, while term policies have set limits—often 10, 20 or even 30 years.

The length you pick should tie directly to your plans and personal finances.

Type of premiums

Life insurance premiums in the UK can be fixed or reviewable. Fixed premiums stay the same throughout your policy term, allowing you to budget with ease and clarity—knowing exactly what you’ll pay each month.

Reviewable premiums start lower but may rise after regular reviews by your insurer; price changes depend on factors like age, health conditions, and market rates.

There is also an option called guaranteed premiums available for whole of life insurance policies.

These remain unchanged throughout your lifetime as long as payments are made on time, giving you certainty in later years without unexpected increases.

Whichever premium type you pick affects how affordable your life insurance cover stays over time.

Additional policy features

Additional features can make a life insurance plan more valuable. Features such as a premium waiver help if you’re ill or cannot work—your payments are covered in tough times.

- Another useful one is terminal illness cover, where the insurer pays out early if you’re diagnosed with less than 12 months to live.

- Some insurers also offer options like children’s cover, giving your family extra peace of mind.

- Policy extras like funeral benefit can help your loved ones quickly access funds for urgent costs after death.

- Indexation features increase your payout yearly in line with UK inflation, keeping up with rising living costs and future needs.

Guaranteed insurability options allow you to raise your coverage without further medical checks after life events, such as marriage or having kids—a convenient feature during key milestones in life insurance planning.

Interested in comparing different types of plans against each other?

The Insurance Hero team has written carefully researched guides explaining the pros and cons of different types of coverage.

This should help you decide on the best action plan for your and your family’s needs.

- Death in Service vs. Life Insurance: Death in service is a workplace benefit that pays a lump sum if you die while employed, whereas life insurance is a personal policy you control and pay for.

- Whole vs. Term Cover: Whole life cover lasts your entire life and has a guaranteed payout, while term cover only pays out if you die within a set period.

- Life vs Critical Illness: Life insurance pays out when you die, but critical illness cover pays out if you’re diagnosed with a serious illness during the policy term.

- Life Insurance vs Mortgage Cover: Life insurance offers flexible financial protection for loved ones, while mortgage cover is tailored to pay off your mortgage if you die.

Every policy has strengths and limits, depending on your lifestyle and needs. Check details carefully, such as premium types, length of coverage, and extra features.

With careful thought, choosing the right life insurance gives peace of mind for life’s surprises ahead.

Resources we consulted

- https://www.moneyhelper.org.uk/en/everyday-money/insurance/what-is-life-insurance

- https://www.abi.org.uk/products-and-issues/choosing-the-right-insurance/life-cover/

- https://www.royallondon.com/guides-tools/life-insurance-guides/types-of-life-insurance/

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.