Life Insurance For Over 55 With No Medical Exam

The 55th birthday is an excellent time to consider life insurance if the cover is not already in place.

A warm welcome to our life insurance for over 55 guide, recently updated for 2025.

Life insurance policies created for people older than 55 make the cover more affordable. When determining premiums, people over 55 are grouped, eliminating the assessment of individual risk.

Life Insurance Over 55: No Medicals Required

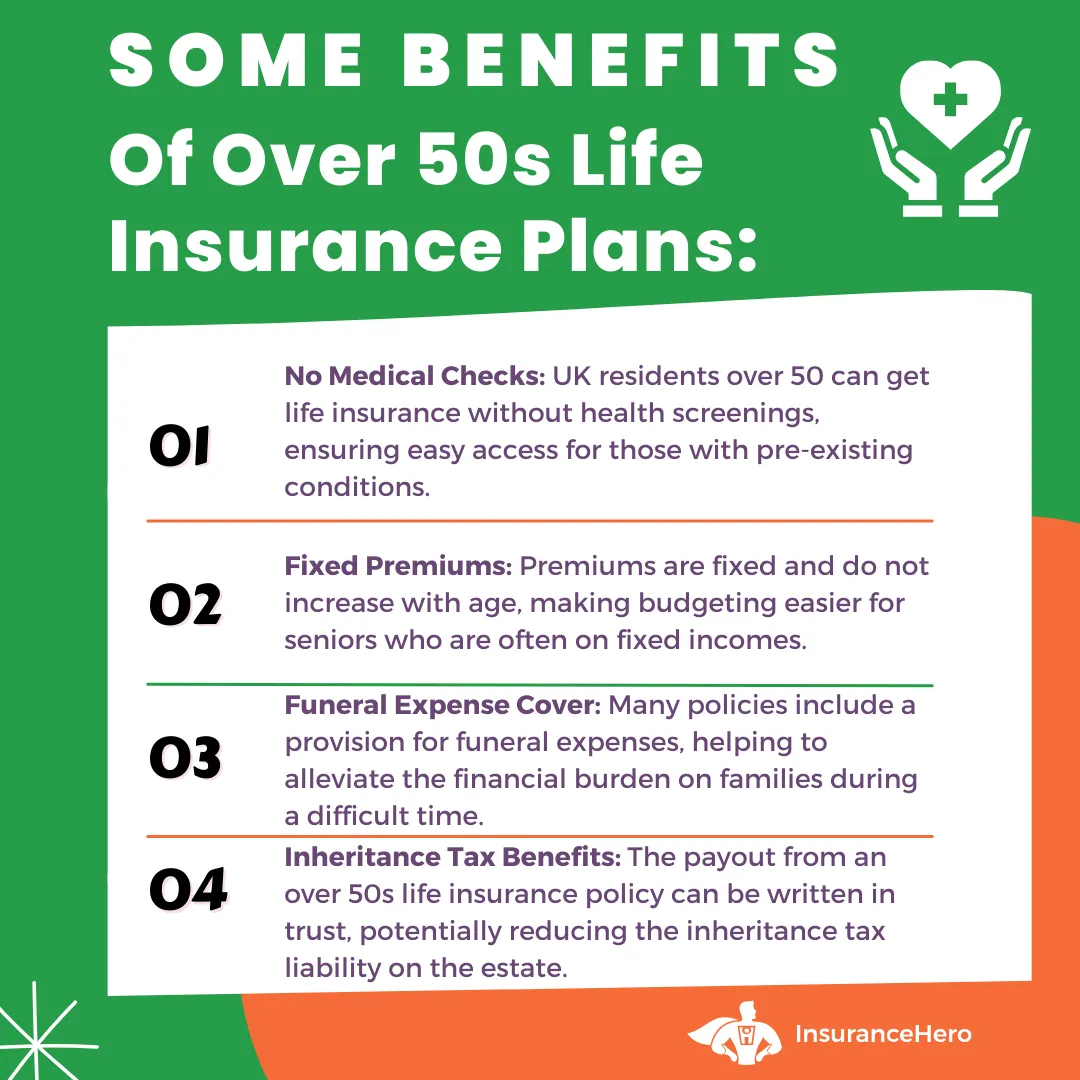

Over 55 life policies do not require medical examinations, so acceptance is guaranteed if the applicant meets the UK residency and age requirements.

Most providers offer guaranteed acceptance through age 75; some even extend this to age 85.

People 55 or older can provide beneficiaries with financial security regardless of their medical condition. This may seem insignificant now, but it can make a huge difference to surviving loved ones.

Aged 55 Or Over And Need Cover? Compare The Leading Life Insurance Companies Below – No-Obligation

Ten reasons to consider life insurance for over 55 cover

- Your children are your financial legacy, so they should be a priority

- You need to provide for your loved ones in the event of your passing

- A life insurance policy will not only pay out a lump sum but will also provide for payments for your dependents for years to come

- You could end up paying a lot of money for medical treatment, so you need to protect your family in case this happens

- It would be best if you started thinking about life insurance as soon as you are married

- It would be best if you did not wait until you are past 55 to think about buying life insurance. Now is the best time

- Life insurance will help your family to pay your debts after your death

- You can protect yourself and your family in case of an accident

- Your life expectancy is more likely to be shorter than other people

Life insurance over 55 premiums are based on smoking status, cover limits, and age at the time of application.

If the insured continues to make premium payments until the stipulated age, the policy will pay a lump sum when the individual dies.

If premium payments cease before that time, coverage will be cancelled, and premiums paid will not be refunded. Therefore, budgeting for this expense over the long term is essential.

Life Insurance and Estate Planning for Over 55s

Life insurance can be crucial in estate planning for those over 55. Here’s how:

- Providing Liquidity: Life insurance can provide immediate cash to cover estate taxes, preventing the need to sell assets.

- Equalizing Inheritances: Life insurance can provide equal value to others if you’re leaving a business or property to one heir.

- Charitable Giving: Life insurance can be used to leave a legacy to a favourite charity without diminishing the inheritance for your family.

- Covering Final Expenses: Ensures your funeral and any outstanding debts are covered without burdening your family.

Integrating life insurance into your estate plan can help ensure that your wishes and those of your loved ones are fulfilled after you’re gone.

Decisions to Make When Considering Over 55 Life Cover

The process of purchasing life insurance when you are single is relatively straightforward. It becomes a bit more complex for married individuals.

Spouses over 55 can buy a joint whole life or term policy, or each person can purchase an individual over 55 policy.

An individual policy is usually more expensive, but it carries several benefits. While a joint policy pays out only once and is then cancelled, each policy carries a payout, so a named beneficiary will receive two payments. This makes individual policies attractive options for parents.

An individual life insurance policy for people over 55 can also be tailored to the policyholder. If one spouse earns more money than the other, this individual can purchase a higher level of cover.

This allows the other spouse to minimize costs while securing cover that benefits survivors.

Couples with children should ensure their limits cover education and future expenses the younger generation will encounter.

Some people over 55 forego this coverage because they receive death-in-service benefits from their employers.

Death-in-service benefits last only while the company employs the individual, and the limit may not be enough to support survivors.

Waiting to secure cover will only make it more expensive. Therefore, people who are older than 55 should make life insurance a priority. Fortunately, Insurance Hero makes this easy to do.

Potential Drawbacks Of Over 55 Policies

Most products have conditions, and life insurance over 55 is no exception. The initial one to two years of coverage is considered a claims blackout period, so if the insured dies, a payout will not be made unless the death was accidental.

The insurer determines the length of this claim-free period, so consumers should review this when comparing policies.

Some insurers provide financial compensation if the insured dies during the blackout period by refunding the premiums paid. Even this small amount of money can go a long way.

Since this insurance is designed for people older than 55 and a medical examination is not required, premiums are higher than those paid by younger individuals in good health.

The premium payment could exceed the policy benefit if the insured lives to age 80 or older.

Cancellation of the life cover does not entitle the former insured to a refund of premiums, and beneficiaries will not receive a payout if the individual dies after the cover is terminated.

Consider life insurance coverage from a lifelong perspective when determining whether it is necessary. The financial security provided to loved ones makes this cover worthwhile for many people.

Beneficiaries can use the money to pay the mortgage, repay debts, cover final expenses, and help with ongoing bills. They can keep their savings intact and might even have extra money to invest or create a nest egg.

Common Misconceptions

Several myths often deter people over 55 from considering life insurance:

Myth 1: It’s too expensive.

Reality: While premiums are higher than for younger people, affordable coverage options are still available.

Myth 2: I’m too old to qualify.

Reality: Many insurers offer policies for people well into their 70s and even 80s.

Myth 3: I don’t need it if I don’t have dependents.

Reality: Life insurance can still be valuable for estate planning, charitable giving, or covering final expenses.

Myth 4: My health issues disqualify me.

Reality: While health affects premiums, many conditions are insurable, and some policies don’t require medical exams. Understanding these misconceptions can help you make a more informed decision about life insurance.

Critical Illness Cover: A Complement To Life Insurance For Over 50s

Critical illness coverage can be a valuable addition to your life insurance policy, especially for those in their fifties. This coverage provides a tax-free lump sum if you’re diagnosed with a specific serious illness covered by the policy.

Commonly covered conditions include:

- Heart attack

- Stroke

- Cancer

- Multiple sclerosis

The benefits of adding critical illness cover include:

- Financial support during recovery

- Covering medical expenses not covered by the NHS

- Allowing you to focus on recovery without financial stress

While it increases your overall insurance costs, the peace of mind and financial protection it offers can be invaluable.

Shopping for Life Insurance Over 55

Life insurance becomes more expensive as we age because claims are more likely. Someone with health issues may find it even more expensive to purchase a life policy.

Unfortunately, one in five retirees in the United Kingdom is below the poverty line, so it may be challenging to afford that as time passes.

However, several companies offer life policies to UK residents older than 55. Rates vary by provider, so consumers should shop for the best deal.

Using the Insurance Hero website, they can save time and effort because we do the work. We scan the market and return rates from multiple insurers, making it easy for consumers to compare offerings.

Our network includes the best life insurance for over 55 companies in the industry, and our technology enables us to search hundreds of policies quickly. You receive free quotes to compare and find the best deal.

Premiums for life insurance for people over 55 begin at just £5 a month. Using our site removes the pressure and obligation of shopping directly with an insurance company.

Our representatives have years of industry experience, so they will happily answer questions and provide more information about this unique type of life insurance.

Once they have reviewed our free quotes, shoppers can rely on us to help them complete the required documents.

We assist every step of the way, removing the confusion and frustration that often results when purchasing life insurance elsewhere.

The new policy becomes effective once the application is approved and remains in force as long as premium payments continue.

There is never a wrong time to buy life cover over 55, and Insurance Hero simplifies the process. We work directly with life insurance companies that offer guaranteed acceptance policies to UK residents older than 55.

By shopping on our site, these individuals receive multiple quotes quickly, allowing them to find the best life cover deals that will financially protect their beneficiaries.

Few things provide the peace of mind that life insurance does, and we make it fast and easy to find an affordable policy.

Reviewing and Updating Your Life Insurance Policy

Life doesn’t stand still, and neither should your life insurance coverage. Regular reviews are essential, especially for those over 55.

Regular reviews ensure your life insurance continues to meet your needs and those of your loved ones.

Consider reviewing your policy:

- Annually

- After major life events (marriage, divorce, birth of grandchildren)

- When your financial situation changes significantly

During your review, consider:

- Is your coverage amount still adequate?

- Are your beneficiaries up to date?

- Has your health improved, potentially qualifying you for better rates?

- Do you need to add or remove any riders?

Case Studies: Real-Life Examples of Life Insurance Benefits for Over 55s

Case Study 1:

Richard, who is 58, took out a £200,000 term life policy to cover his mortgage. When he unexpectedly passed away at 65, the policy paid out, allowing his wife to clear the mortgage and maintain her standard of living.

Case Study 2:

Lisa, 57, chose an AIG whole life policy with critical illness cover. At 65, she was diagnosed with cancer. The critical illness benefit helped cover her treatment costs and loss of income during recovery.

Case Study 3:

Daniel, 62, used life insurance as part of his estate planning. He placed his policy in trust and ensured his children received the full benefit without inheritance tax implications.

These examples illustrate how life insurance can provide crucial financial support in various scenarios for people in their fifties.

Healthy Ageing Tips For The Over 50s

Adopting healthy habits in your fifties, such as regular exercise, a nutritious diet, social engagement, and routine medical check-ups, can significantly enhance a person’s quality of life and independence as one ages.

Is Life Insurance Cover Worth It After The Age Of 50?

Although it might cost more as you age, over-50s coverage can still be valuable for covering end-of-life expenses, leaving a financial gift, or helping family members manage debts or funeral costs.

Over 50 Life Insurance vs Funeral Plans

Over 50 life insurance provides a guaranteed cash payout that can be used for any purpose. At the same time, funeral plans are designed to cover specific funeral services and may offer less flexibility in how the funds are used.

Our “Is life insurance better than a funeral plan guide?” goes into more detail, explaining the pros and cons of each.

Over 50 Life Insurance Average Cost

The average monthly cost of over-50s life insurance varies based on factors like age, health, and coverage amount, with typical premiums starting from around £10–£30 per month for fixed-benefit policies.

Steve Case is a seasoned professional in the UK financial services and insurance industry, with over twenty years of experience. At Insurance Hero, Steve is known for his ability to simplify complex insurance topics, making them accessible to a broad audience. His focus on clear, practical advice and customer service excellence has established him as a respected leader in the field.